By Sam L. Savage

A combination of the war in Iran, which has roiled petroleum prices, and AI Data Labs that have increased demand for electricity, have led to tremendous uncertainty in energy investments.

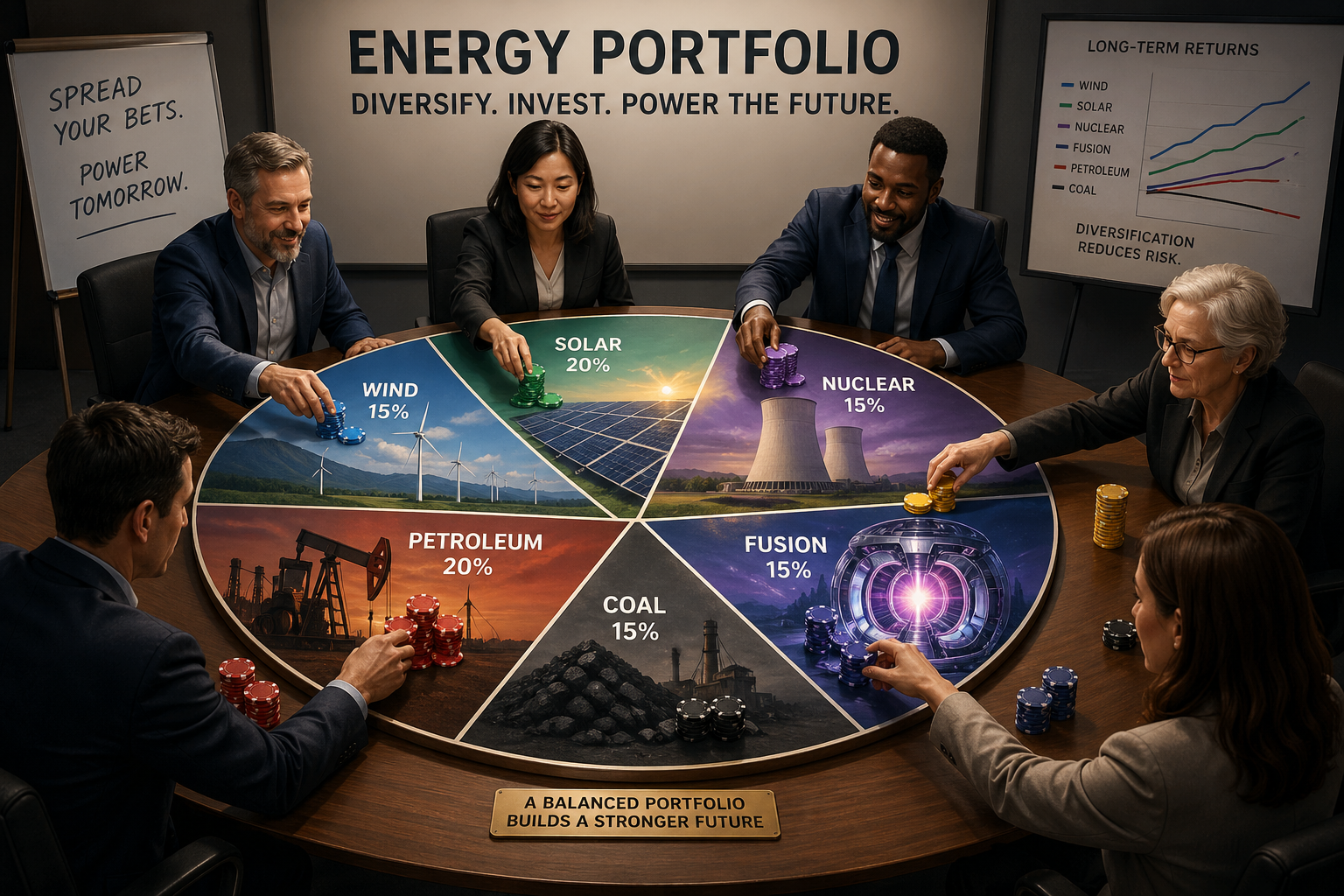

I urge you to read Deborah Gordon’s article on portfolios of energy investments for the GFCC (Global Federation of Competitiveness Councils). I have known Deborah for many years, and she is a valued member of my Board of Directors at the nonprofit. Her article highlights the necessity of quantifying uncertainty in one of humanity’s highest priorities: producing energy. Deborah and I have discussed at length the application of portfolio theory at Royal Dutch Shell to optimal exploration sites, which ultimately led to the formation of ProbabilityManagement.org. Where at Shell, we focused on portfolios of individual projects in the face of uncertain prices, Deborah zooms out to portfolios of energy types, wind, solar, petroleum, coal, nuclear, and fusion in the face, not only of price uncertainty, but major geopolitical and technological uncertainties as well.

The methods we applied at Shell were based on coherent stochastic data, pioneered by financial engineers of the 1980s. Today this approach has been greatly improved in our Open SIPmath™ 3.0 Standard, developed in connection with Doug Hubbard, Tom Keelin, and Frontline Systems, and it is the ideal basis for tackling the energy portfolio problem described by Deborah. For a simple example, see our portfolio of wind and solar on our Renewable Energy page.

Copyright © 2026 Sam L. Savage